- Gary Antonacci popularized dual momentum with an effective and simple approach for dynamic asset allocation: Global Equities Momentum (GEM).

- Using simulated ETF data series, GEM’s performance over past market conditions can be approximated.

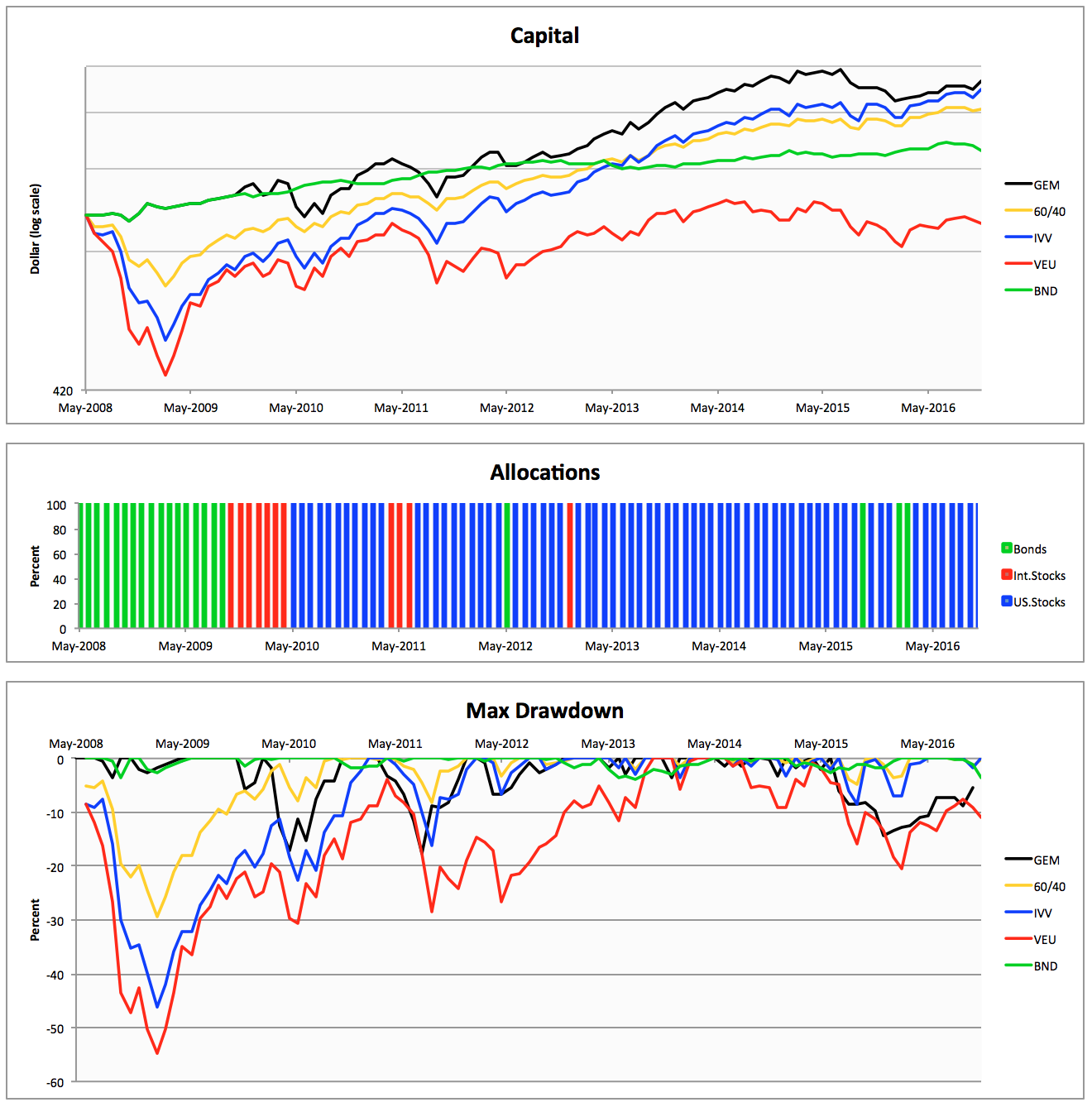

- For longer investment horizons GEM’s implementation with ETFs obtained positive returns with high consistency.

After winning first place in 2012 in the

NAAIM Wagner competition, Gary Antonacci popularized his momentum investing approach in the award winning book “Dual Momentum Investing”.

In his book Antonacci makes a strong case for combining relative strength price momentum with trend following absolute momentum. The first 90 pages are a comprehensive overview, introducing the “premier market anomaly”, describing the history of momentum research and its early practitioners, behavioristics and lots of other interesting themes. Frankly, these pages alone make the book a must read, not least due to the conversational, at times even playful tone of Antonacci’s light pen.

At the center of the book lies the chapter covering Global Equities Momentum (GEM), where Antonacci explains the mechanics of the dual momentum approach for dynamic asset allocation. GEM is quite brilliant in its simplicity: a 12-month lookback for both absolute and relative momentum combined with just three asset classes, are all of GEM’s components.

Both in his book and on his

website, Antonacci presents the Global Equities Momentum (GEM) approach with non-tradable total return index data. Going back as far as the seventies has the benefit of incorporating a rising yields decade too. Therefore, to get insight into GEM’s long-term performance with today’s ETFs, index based simulated total return proxies are required. By applying GEM’s dynamic asset allocation to such simulated ETFs, the practitioner may get a good impression (nothing more) of GEM’s “real” performance during past market conditions. Before doing so, first GEM’s performance with index data will be replicated to validate the accuracy of the presentation in this contribution.

Noteworthy, the rules often shared for GEM, derived from the flow chart on page 101, are

not the official GEM rules. Actually the flow chart along with the corresponding instructions on page 112 is only a simplified way to determine GEM’s allocations for those using a website like

PerfCharts to get their signals. However, when doing calculations with a charting program like

AmiBroker, the instructions on page 98 are to be adhered instead.